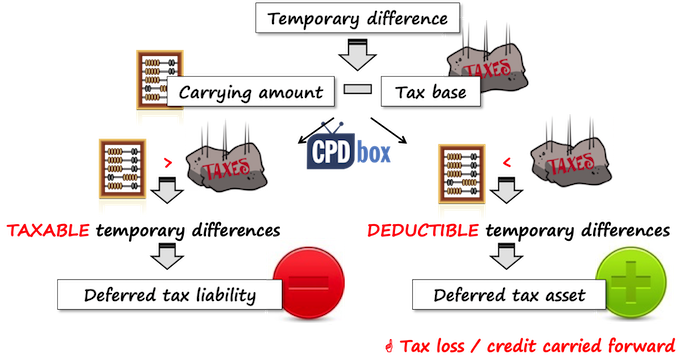

Temporary differences are differences between the carrying amount of an asset or liability in the statement of financial position and its tax base IAS 125. The recoverability of deferred tax assets where taxable temporary differences are available.

Temporary Differences In Tax Accounting Dummies

There was an outcry about this approach and so the now defunct Accounting Standards Board ASB required this particular area to be redrafted but to be as near to the international equivalent IAS 12 Income Taxes as possible.

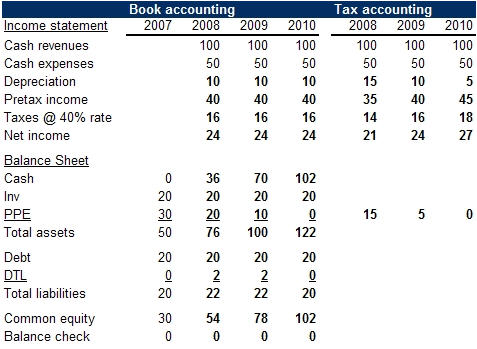

Deferred tax temporary differences. Table 1 shows the carrying value of the asset the tax base of the asset and therefore the temporary difference at the end of each year. Permanent Differences Temporary differences. Deferred tax assets for deductible temporary differences arising from investments in subsidiaries branches and associates and interests in joint arrangements are only recognised to the extent that it is probable that the temporary difference will reverse in the foreseeable future and that taxable profit will be available against which the temporary difference will be utilised.

The temporary taxable difference ie. Deferred tax is the amount of tax payable or recoverable in future reporting periods as a result of transactions or events recognised in current or previous periods accounts. Therefore the entity recognises a deferred tax asset of 25 100 at 25 provided that it is probable that the entity will earn sufficient taxable profit in future periods to benefit from a reduction in tax payments.

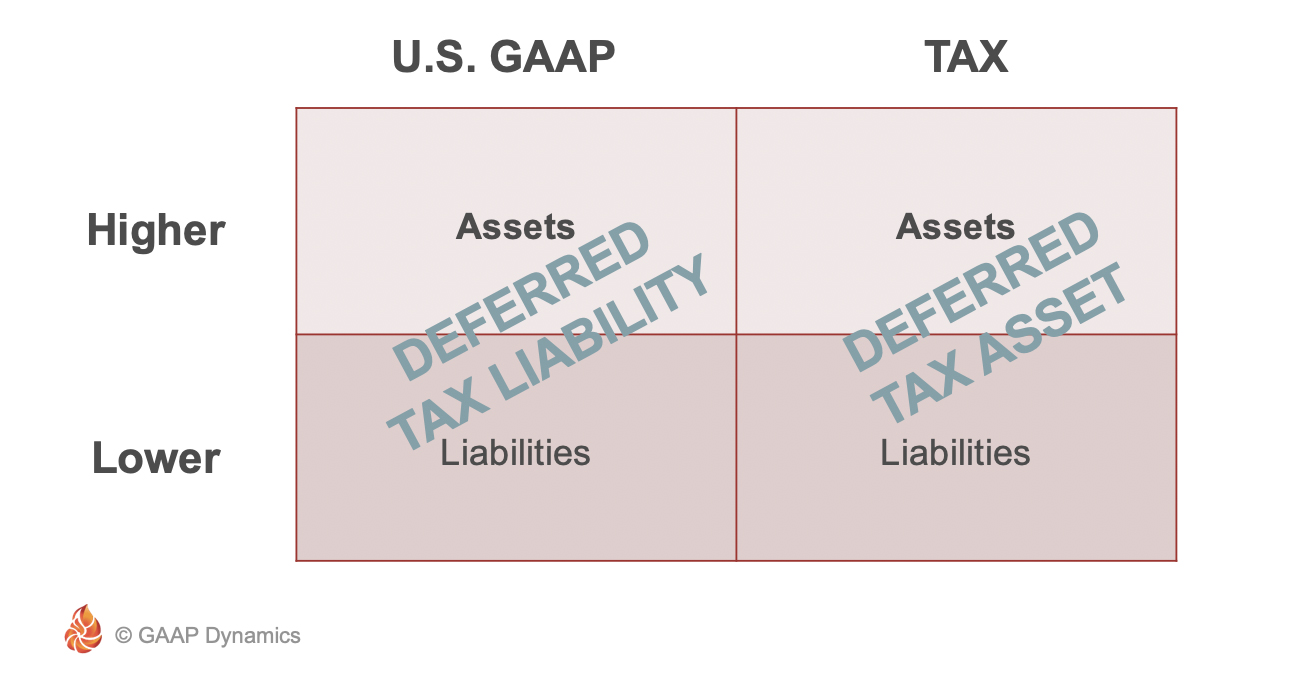

As stated above deferred tax liabilities arise on taxable temporary differences ie those temporary differences that result in tax being payable in the future as the temporary difference reverses. Temporary Differences Taxable temporary differences. The notion of temporary differences is fundamental to understanding deferred tax.

Likewise a temporary difference will make the net income before tax in the accounting base different from taxable income following the tax base. Because of these inconsistencies a company may have revenue and expense transactions in book income for 2013 but in taxable income for 2012 or vice versa. If a temporary difference causes pre-tax book income to be higher than actual taxable income then a deferred tax liability is created.

A a deferred tax asset for temporary differences that will reduce taxable profit deductible. Deferred Tax arises from the temporary differences. Current tax vs deferred tax.

As a result it creates deferred tax which could be deferred tax asset or deferred tax liability. As mentioned earlier in the article the previous FRED 44 required deferred tax to be computed using a temporary difference approach. This creates a temporary positive difference between the companys accounting earnings and taxable income as well as a deferred tax liability.

Temporary differences may impact on financial statement because of income and expenses appear within one accounting period but the tax payable in a different accounting period. Temporary difference is the difference between the value of an asset or liability in the balance sheet following the accounting base and its tax base. The difference between the carrying amount of 100 and the tax base of nil is a deductible temporary difference of 100.

For many entities deferred tax assets can be recognised for non-capital losses but only when supported by convincing evidence that future taxable profit exists. The difference in carrying value of the asset and the tax base value has fallen to 50k resulting in a deferred tax liability of 95k 50k 19 corporation tax rate. Generally FRS 102 adopts a timing difference approach ie deferred tax is recognised when items of income and expenditure are.

In other words temporary differences are timing differences with respect to recognition of transactions in IFRS financial statements and for tax purposes. Temporary differences occur because financial accounting and tax accounting rules are somewhat inconsistent when determining when to record some items of revenue and expense. Taxable temporary differences are timing differences which cause taxable income in.

Deferred tax refers to income tax overpaid or owed due to the temporary differences between accounting income and taxable income. This is because the company has now earned more revenue in its book than it has recorded on its tax returns. For an established business with a long history of profitability deferred tax assets are often recognised without debate for deductible temporary differences that exist at each reporting date.

As stated above deferred tax liabilities arise on taxable temporary differences ie those temporary differences that result in tax being payable in the future as the temporary difference reverses. It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time. Differences are known as temporary differences because they will eventually reverse when the company recovers the asset or settles the liability.

Temporary differences occur when a business has an asset with a liability value that does not match with the current taxable value of the asset. Take the Next Step to Invest Advertiser Disclosure. The reversal of temporary differences will either increase or reduce taxable profit.

The recognition of deferred tax assets is subject to specific requirements in IAS 12. A temporary difference however creates a more complex effect on a companys accounting. Deductible temporary differences are differences which cause the taxable income and.

Temporary differences are usually calculated on the differences between the carrying amount of an asset or liability recognized in the statements of financial position and the amount attributed to that asset or liability for tax at the beginning. Table 1 shows the carrying amount of the asset the tax base of the asset and therefore the temporary difference at the end of each year. The formation of deferred tax assets or liabilities from temporary differences can only occur if the differences reverse themselves at some future date and to such an extent that the balance sheet items are expected to create future economic benefits for the company.

Temporary difference do give rise to potential deferred tax but the rules on whether the deferred asset or liability is actually recognised can vary. Deferred tax assets are recognised only to the extent that recovery is probable. Two types of temporary differences.

Deferred Tax Asset Temporary Difference Revenue Or Expense Taxable Income Lower Than Book Youtube

2021 Cfa Level I Exam Cfa Study Preparation

Pdf Effect Of Temporary Differences On Deferred Tax In The Banking Sector In Rwanda

Deferred Taxes Modeling Deferred Taxes Wall Street Prep

Ias 12 Income Taxes Cpdbox Making Ifrs Easy