An Auditor also needs to ensure whether the books of accounts show a true and fair view of the state of affairs of the company or not. The auditors responsibilities for the engagement will mean that detection of those types of irregularity which give rise to a risk of material misstatement are those on which the auditor is able to provide the most comprehensive explanation.

Pdf Frauds And Errors In The Audit Of Financial Statements

Even a simple hint that.

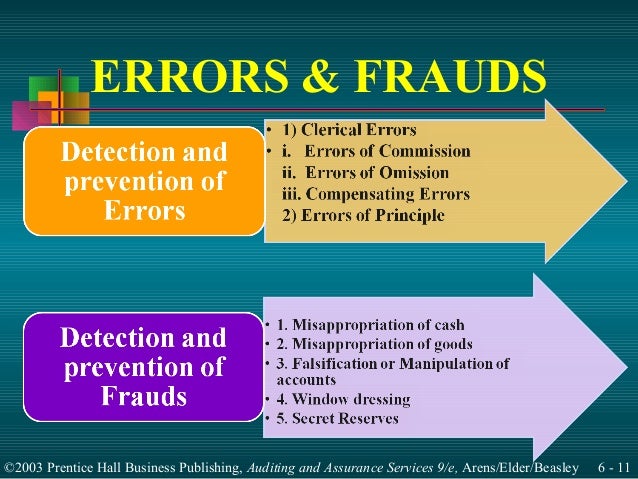

Errors and frauds in auditing. Errors on the other hand may creep in accounts due to omission or clerical errors on the part of employees. The auditor seeks reasonable assurance that fraud or error which may be material to the financial statements has not occurred or if it has occurred that the effect is properly reflected in the financial statements. Fraud can take the form of the falsification or alteration of accounting records or the financial statements.

He should fulfil his duty as per the prevailing standards of his profession. Auditor Responsibility for Errors and Fraud Auditing and Attestation CPA Exam - Duration. Detection of fraud is just an incidental object.

Audited account are detected as an authentic record of transaction. An error represents an unintentional misstatement of the financial statement. The distinguishing factor is whether the underlying action that resulted in the misstatement was intentional or unintentional.

ISA 240 the Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements recognises that misstatement in the financial statements can arise from either fraud or error. Errors may classified as. Abstract Responsibility for preventing and detecting fraud rest with management entitiesAlthough the auditor is not and cannot be held responsible for preventing fraud and errors in yourwork he.

Fraud represents an intentional misstatement of the financial statement which can be material or immaterial. Errors and frauds are detected and rectified. Include errors that occur and not have an impact on the balance of the trial balance in the sense that these errors even though they occur the trial balance equal both in the total debits and credits or in total accounts payable and total accounts receivable could happen this kind of errors in the following types.

So is intentionally booking a lower allowance for bad debt than is deemed reasonable by normal estimation methods. The auditors duties for the prevention detection and reporting of fraud other illegal acts and errors is one of the most controversial issues in auditing. Prevention of Errors and Fraud An Auditor should audit as per the principles laid out for auditing.

Because of his expertise the auditor may advise on various matters to his clients. For the auditor prevention and detection of errors and fraud is only a secondary objective. Auditing is the examination of accounting books documentary evidences through which an.

The main objective of auditing is to ensure the financial reliability of any organization. This evidence supports the audit. It increases the morale of the staff and thus it prevents frauds and errors.

Fraud may be perpetrated by manipulation of accounts. The role of the auditor in discovering error fraud and illegal behavior in the financial statements. Errors The term error in audit context refers to unintentional mistakes in the preparation or presentation of financial information.

Meaning Objectives Errors and Frauds Definition of Auditing. Frauds throughout the conduct of his audit task. It may be material or immaterial.

The objectives of an audit may broadly be classified as Primary objectives and Secondary. At the very outset it would be apt to remark that errors generally arise out of the innocence or carelessness on the part of those responsible for the preparation of accounts while fraud involves some intention to gain out of manipulating records. Independent opinion and judgement form the objectives of auditing.

Errors are not shown by the trial balance. AAS 4 Auditors Responsibility to Consider Fraud and Error in an Audit of Financial Statement1 states that errors are unintentional misstatement or. Inherent limitations of an audit.

Farhats Accounting Lectures 9595 views. Misapplication of accounting policies unknowingly. An auditor should assess the risk that may occur from the existence of errors or manipulation that clearly affect the financial statements in the companies or establishments they are auditing because it is the main reference for them in the auditing plan and the design of testing program.

Irregularities that result from fraud might be inherently more difficult to detect than irregularities that result from error. Deliberately making a mistake when coding expense checks is fraud. The job of an Auditor is to ensure that the books of accounts are kept according to the rules stipulated in the Companies Act.

Given the signal indicators of the risk of fraud the auditor should use the best procedures through which to obtain sufficient and appropriate audit evidence. Error should be rectified during his audit and fraud is to be reflected in his audit report.