This video shows how to apply the lower-of-cost-or-market rule to value inventory. In the context of inventory valuation and lower of cost or market net realizable value takes on a meaning very specific to inventory.

Solved Brief Exercise 6 7 Your Answer Is Incorrect Blue Chegg Com

Lower-of-cost-or-market valuation is a method that is calculated as taking the lower number of.

Compute the lower of cost or market valuation. Determine the market value or expected selling price of an asset. Lower of Cost and Net Realizable Value LCNRV Rule Like many other assets inventory is recorded and reported at cost in accounting books following historical cost principle following a certain cost flow assumption either FIFO LIFO AVCO or other methods. It is defined as the estimated selling price minus all estimated selling costs and costs to complete the product.

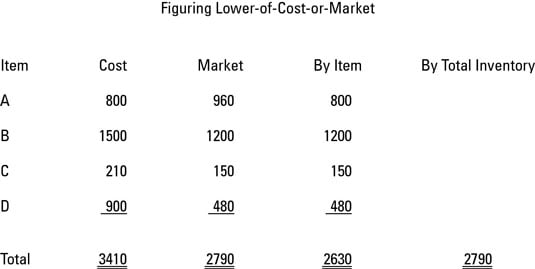

Then the company would record a 400 loss because the inventory has lost some of its revenue-generating ability. However there are times when the original cost of the ending inventory is greater than the net realizable value and thus the inventory has lost value. The first column is the item the second column is the cost and the third column is the market value.

Another way of measuring inventory value is based on net realizable value NRV. The market method assigns a value to your inventory based on what you could get in the market place at the time inventory is counted. Calculate the difference between the market value expected selling price of an asset and the costs associated with the completion and sale of an asset.

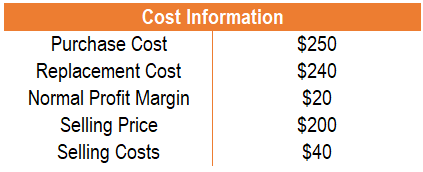

The replacement cost cannot exceed the net realizable value or be lower than the net realizable value less a normal profit margin. It is a net realizable value of an asset. Lower of Cost or Market.

This allows you to discount damaged goods write off obsolete products and adjust your valuation based on the fluctuation of market prices. The lower of cost or market LCM method states that when valuing a companys inventory it is recorded on the balance sheet at either the historical cost or the market value. The difference between cost and market value.

Cost refers to the purchase cost of inventory and market value refers to the replacement cost of inventory. Under LCM inventory items are written down to market value when the market value is less than the cost of the items. The value of the inventory would now be stated in the balance sheet at 75.

Then the company would record a 5000 loss because the inventory has lost some of its revenue generating ability. Find all costs associated with the completion and the sale of an asset cost of production advertising transportation. Since the replacement cost of 880 lies within the limits set by LCM rule it is allowable market value of the inventory.

The numbers in the first line of this. Inventory Categories Cost Data Market Data Cameras 11029 12109 Camcorders 8094 8664 DVDs 11777 10467 Compute The Lower-of-cost-or-market Valuation For Companys Inventory The Lower-of-cost-or-market Value. This market value is to be compared to the original cost of inventory which is 900.

For example assume that the market value of the inventory is 39600 and its cost is 40000. It is noteworthy that the lower-of-cost-or-NRV adjustments can be made for each item in inventory or for the aggregate of all the inventory. For example 1 when we have valued stock at a lower cost or a Market Price of 1000 the Gross Profit is 1500 whereas in example 2 when we have valued stock at a higher cost or a Market Price of 1200 the Gross Profit is 1700.

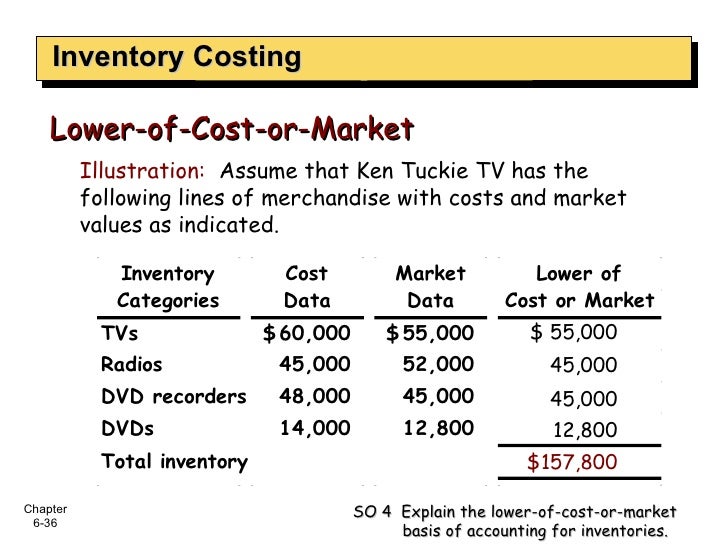

Mathematically the net realizable value can be found through the following equation. Oriole Company Accumulates The Following Cost And Market Data At December 31. Compute the lower-of-cost-or-market valuation for Sadowski inventory.

The lower of cost or market inventory adjustment required in the accounting records to reflect the write down is as follows. Under LCM inventory items are written down to market value when the market value is less than the cost of the items. For example assume that the market value of the inventory is 50000 and its cost is 55000.

In the latter case the good offsets the bad and a write-down is only needed if the overall value is less than the overall cost. Calculate the Lower of Cost or Market As the market value to use is 75 and the cost is 90 the lower of cost and market is 75. A comprehensive example is presented to illustrate how the original cost.

Lower of cost or market LCM is an inventory valuation method required for companies that follow US. Lower Cost or Market Valuation. Since the market value of inventory is lower than its original cost therefore it should be stated at 880 in the financial statements.

15968 12669 17024 total lower of cost or market. Normally ending inventory is stated at historical cost. Lower of cost or market LCM or LOCOM is a conservative approach to valuing and reporting inventory.

Using the lower of cost or market means comparing the market value of each item in ending inventory with its cost and then using the lower of the two as its inventory value.

How To Use Lower Of Cost Or Market Dummies

Ch06

Lower Of Cost Or Market Rule Example Youtube

Financial Accounting Sixth Edition Ppt Video Online Download

Lower Of Cost Or Market Lcm Definition Inventory Valuation Examples